OneStream has become a cornerstone platform for modern FP&A organizations, enabling integrated planning, forecasting, and reporting at enterprise scale. Yet many finance teams still struggle to unlock its full value, not because of limitations in the technology, but because the assumptions feeding their models are incomplete, outdated, or disconnected from how the business actually operates.

As volatility increases and planning cycles compress, FP&A leaders are rethinking how assumptions and operational drivers enter OneStream in the first place. The next frontier of OneStream value creation sits at the intersection of process design, intelligent data ingestion, and continuous planning.

Who This Is For

This perspective is designed for FP&A leaders and finance transformation teams who have already selected or implemented OneStream and are focused on accelerating time to value, improving forecast relevance, and scaling planning capabilities beyond static annual cycles.

For teams earlier in their CPM journey, see our guide on maximizing your CPM investment across Finance and IT.

Below are five proven best practices FP&A organizations are adopting, supported by CrossCountry Consulting and Sensible AI, to move from static planning to adaptive, insight driven decision making within OneStream.

1. Treat Unstructured Data as a Strategic Planning Asset

Many of the most critical planning assumptions don’t originate in financial systems. They live in contracts, pricing schedules, vendor agreements, and headcount files that sit outside OneStream.

Leading FP&A teams design OneStream models around true business drivers and establish scalable ways to transform unstructured source data into inputs that are ready for system use, reducing reliance on spreadsheets and increasing confidence in planning assumptions.

2. Anchor Driver-Based Planning in Real-World Business Signals

Driver based planning is only as effective as the relevance of its drivers. Updating assumptions on a fixed cadence, regardless of how the business changes, limits responsiveness.

High-performing teams connect drivers to commercial and operational signals such as pricing terms, renewals, volume thresholds, and cost escalators, ensuring financial impact is reflected as the business evolves.

3. Make Scenario Modeling Fast, Repeatable, and Scalable

Scenario modeling is essential for executive decision-making, yet many FP&A teams limit scenarios due to the effort required to gather and validate assumptions.

By standardizing scenario frameworks in OneStream and reducing friction in assumption ingestion, FP&A teams can run more best, base, and worst case scenarios per cycle and respond faster to leadership questions.

4. Eliminate Manual Effort to Reinvest in Strategic Analysis

Even mature OneStream environments often rely on manual extraction and spreadsheet-based workarounds that slow planning cycles and introduce risk.

Automating assumption ingestion and standardizing planning workflows frees FP&A capacity for higher-value activities such as variance analysis, business partnering, and strategic storytelling.

5. Shift from Periodic Forecasting to Continuous Planning

Annual planning and static forecasts are no longer sufficient in dynamic business environments.

Leading organizations operationalize continuous planning in OneStream through rolling forecasts supported by continuously refreshed inputs, improving forecast accuracy and decision relevance throughout the year.

What Leading FP&A Teams Measure

FP&A leaders embracing these practices typically track improvements in forecast accuracy, time to update forecasts after assumption changes, number of scenarios modeled per cycle, and manual hours eliminated. More importantly, they see FP&A repositioned as a strategic partner delivering timely, trusted insight when it matters most.

Ready to Unlock More Value from OneStream?

If you’re looking to accelerate OneStream outcomes, modernize your planning operating model, or move toward continuous, driver-based planning, we’d welcome a conversation.

Meet with our team of OneStream and FP&A transformation experts to discuss your goals and identify practical next steps.

Contact us to schedule a conversation.

Regional banking institutions evaluating new ERP or EPM systems often focus on improving how transactions are captured, closed, and consolidated within the Record-to-Report process. When the emphasis centers on general ledger design and system implementation, reporting strategy is frequently addressed too late in the process.

Yet the largest consumers of financial information are rarely considered early in technology design and implementation. Reporting strategies must support regulatory reporting across agencies such as the FDIC, Federal Reserve, and SEC, while also enabling internal management reporting across financial performance and operational activity. When implementations focus primarily on ledger design and transaction processing, the needs of these reporting stakeholders are often addressed too late.

This raises an important question: how should financial institutions design reporting architecture that meets the needs of all stakeholders from the beginning, rather than retrofitting solutions after an implementation is already underway?

The answer is to anchor system design in reporting requirements from the start. Instead of treating reporting as a downstream output of the general ledger or EPM platform, institutions must first define the reports they need to produce—from regulatory filings to board materials and profitability analyses—and then design the supporting data architecture accordingly. While formats may differ, all reporting should be drawn from consistent, multi-dimensional, and governed source data. Without that foundation, even the most advanced platforms simply accelerate existing fragmentation rather than resolve it.

Neglecting Reporting During Implementation

Across institutions, as much as 75% of resource time is spent gathering, reconciling, and validating data rather than analyzing it. Instead of enabling insight and automation, finance teams devote significant effort to manual processes across fragmented data sources simply to produce required reporting.

This misallocation of effort begins with a single misstep: treating reporting as an afterthought. When reporting requirements are not defined upfront, “shadow reporting” is developed to fill the gap. Regulatory, management, and statutory outputs evolve along separate paths, creating data silos without a single version of the truth producing unreliable data and increasing operational reporting risk.

Reversing this pattern requires more than incremental fixes. It requires designing reporting architecture deliberately, with clear multi-dimensional structure, governed data foundations, and defined methodologies from the outset. Only then can institutions redirect effort away from reconciliation and toward insight.

Crafting a Holistic Reporting Strategy

Institutions must also support multiple categories of reporting, including regulatory reporting (SEC, FINRA, FDIC/Federal Reserve), management reporting (business reviews, board reporting, ALCO), and other internal reporting across accounting, tax, credit risk, and operations. While these reports serve different audiences, they are largely derived from the same underlying data at varying levels of granularity.

The starting point for these institutions is to catalog the full inventory of required reporting and define the data outputs necessary to support each use case, with a clear focus on delivering value to the end user. Once defined, the reporting strategy becomes a north star, guiding the evolution of reporting capabilities as well as supporting data and technology infrastructure. When aligned properly, this foundation enables institutions to meet all reporting needs from a single version of the truth, driving consistency, efficiency, and more meaningful insight.

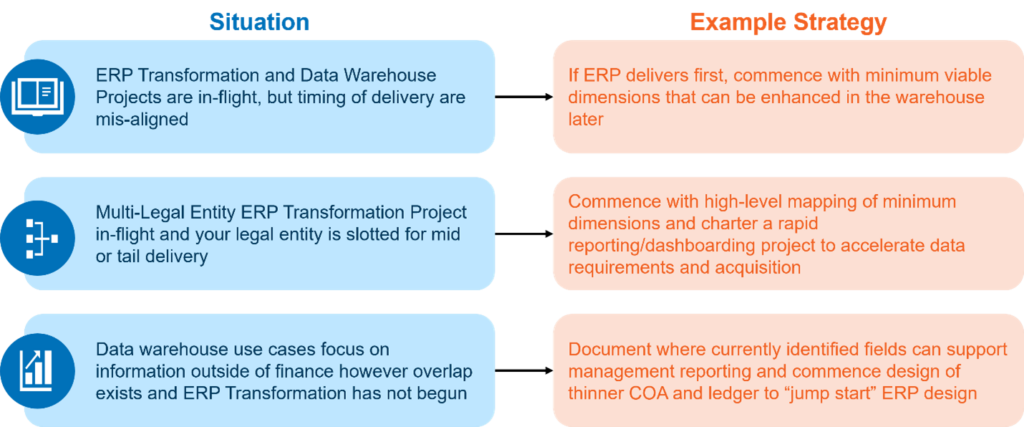

When planning a reporting strategy, it is important to consider the different timing scenarios that may arise. An example of common situations and related strategies include:

It’s not uncommon for institutions to define target and interim states to deliver value on an incremental and manageable basis. Typical timelines range from 3-24 months, delivering notable functionality on a quarterly/semi-annual basis.

Single Version of The Truth

Achieving a single version of the truth begins with rethinking the data foundation. While the general ledger is essential for financial reporting, it is inherently too summarized to support deeper strategic insight.

The path forward is to establish an instrument-level foundation that captures transaction detail at its natural level of granularity, including loans, deposits, securities, and other financial products. From there, dimensions must be harmonized across the enterprise so that regulatory and management reporting draw from the same governed data source.

When reporting frameworks originate from a common foundation, reconciliation becomes embedded in the architecture rather than dependent on manual effort. The result is a reporting environment that supports statutory requirements while remaining flexible enough to generate meaningful business insight.

Optimizing Reporting for Strategic Insights

Once the data foundation is in place, the focus shifts from assembling numbers to generating insight. For regional banks and diversified financial institutions, this means moving beyond static P&L statements toward multi-dimensional reporting.

The most meaningful insights emerge when performance can be evaluated across consistent enterprise dimensions. At a minimum, institutions should be able to analyze activity by Customer or Client, Product, Account, Organization, at the Instrument level, and at intersections across enterprise dimensions. By examining these dimensions, leaders not only gain insight into the numbers themselves but also uncover the reasons behind their changes and identify where genuine value is generated.

Achieving this requires more than layering attributes onto the general ledger. Each dimension must be defined, governed, and structured hierarchically so that activity rolls consistently from instrument to product, product to line of business, and into enterprise reporting without manual reclassification. When that structure is in place, finance, risk, treasury, and regulatory reporting can view the same activity through different lenses.

That is what transforms reporting from a compliance obligation into strategic analytics that drive business objectives.

The Reporting Landscape

Financial institutions operate in one of the most complex reporting environments of any industry. Regulatory filings, statutory financials, and internal management reporting each impose distinct structural requirements and levels of granularity, and none map cleanly across reports or to the general ledger. Regulatory reports such as the Federal Reserve Y-9C or FDIC Call Report require highly specific classifications and cross-report integrity, while management reporting demands flexible views across clients, products, segments, and business lines.

These requirements rarely align naturally with the structure of the general ledger chart of accounts. Without intentional design, institutions typically resort to developing parallel reporting processes for regulatory, statutory, and management outputs, increasing reconciliation effort and operational risk.

The objective of a modern reporting architecture is not to eliminate multi-dimensional reporting differences, but to anchor them to a common data foundation. When reporting frameworks draw from the same governed source of instrument-level data, institutions can satisfy multiple reporting obligations while preserving transparency, consistency, and reconciliation across report outputs. The same loan can satisfy a Call Report schedule, an FRB submission, or an SEC maturity bucket disclosure simply by applying the right attribution logic — no separate pipelines required.

This foundation becomes especially important when management reporting evolves beyond financial statements into profitability and performance analytics.

The Role of Management Accounting Methodologies

With a consistent reporting architecture in place, institutions can move beyond producing numbers to understanding performance. This is where management accounting methodologies become critical.

Multi-dimensional profitability and planning are only as credible as the methodologies that support them. When poorly designed or inconsistently applied, business lines lose confidence in the numbers, and management reporting stops driving decisions. Four areas consistently distinguish institutions that generate meaningful insight from those that do not.

Funds Transfer Pricing (FTP)

Without a disciplined FTP framework, business lines appear more or less profitable than they actually are. FTP transfers interest rate and liquidity risk to a central function where it can be properly managed, leaving business lines with a stable, comparable margin that reflects true commercial performance.

Expense and Cost Allocation

When costs are not allocated to the deal or instrument level, product profitability becomes guesswork and accountability breaks down. A well-designed allocation model assigns costs based on actual consumption and rolls them into meaningful product and business-line views. Whether an institution allocates fully or excludes corporate overhead matters less than making that decision deliberately and applying it consistently.

Revenue Sharing and Allocation

In relationship-driven institutions, deals frequently involve multiple teams. When attribution rules are not defined upfront, disputes inevitably follow. Upfront sharing, ongoing splits, and double-counting each create different behavioral incentives and reporting outcomes. Establishing clear governance around revenue attribution is therefore as much a cultural decision as a technical one.

Capital Allocation

Business lines that do not bear the cost of capital have little incentive to use it efficiently. Allocating regulatory capital to products and lines of business, and measuring returns against that cost, allows institutions to evaluate performance in terms of shareholder value rather than revenue alone. As with other management accounting methodologies, capital allocation must balance analytical precision with decision-making value and long-term maintainability; excessive granularity can add complexity without improving insight.

Governance and Transparency

The fastest way to undermine any of the accounting methodologies is opacity. When business lines cannot explain how allocations are calculated, they quickly stop trusting the results. Tying charges to understandable activity drivers—accounts serviced, transactions processed—transforms allocation from a political debate into a practical tool for running the business.

Technology-Enabled Reporting Done Right

The journey to optimized reporting and analytics is not simply a technology upgrade. By building reporting frameworks rooted in instrument-level data, governed multi-dimensional structures, and disciplined management accounting methodologies, regional banking institutions transform how the finance function operates and delivers value to the organization.

Teams that once spent as much as 75% of their time gathering and reconciling data can redirect that effort toward generating insight and informing decisions. For institutions seeking to scale, this shift represents a meaningful and sustainable competitive advantage.

The institutions that define their reporting and analytics strategy at the beginning of a transformation position themselves to extract far greater value from ERP and EPM investments. CrossCountry Consulting helps financial institutions develop these strategies to deliver scalable insight, stronger governance, and long-term business value.

Migrating off SAP ECC and on to S/4HANA in the near future? SAP maintenance of ECC is sunsetting in 2027, with some support available into 2030. Don’t underestimate the time and complexity involved.

Most organizations materially under-budget and under-plan their S/4HANA transformations because they anchor on software and system integrator costs while underestimating internal effort, data complexity, and operating model change. Now’s the time to set up your organization for success and lay the foundation for an efficient, profitable transition.

Here’s where to begin.

Phase 1: Strategic Planning, Project Budgeting, and Migration Planning

Timeline: 3–6 Months

Goal: Define the “What,” “Where,” and “How Much.”

1. SAP Readiness Check (Technical Foundation)

Before you budget, run an SAP Readiness Check. It provides:

- Simplification items: Which ECC functions are deprecated or changed in S/4HANA.

- Custom code impact: An automated scan of your custom “Z” objects to identify incompatibilities with S/4HANA and expose embedded technical debt that must be remediated, retired, or redesigned.

- Sizing recommendations: The HANA memory requirements (this dictates your cloud/hardware costs).

- Data readiness assessment: Existing database and data structures can have a big implication on the transition timeline, data strategy, and transition options. If data isn’t in a unicode format, doing a Brownfield RISE conversion is more complex compared to a Greenfield GROW conversion where there is no impact.

2. Architecture Decision and Hosting Model

Decide between SAP RISE versus GROW. Each has public vs private cloud options and slight functionality differences. From there, various kinds of bundling, licensing, and management options are available.

Note: With GROW, you can only do Greenfield implementations; with RISE, you can do Greenfield, Brownfield, or Bluefield (see below).

Featured Insight

3. Selection of Migration Strategy (The ‘Big Three’)

You must choose your path now, as it can change the budget by millions:

- Greenfield (new implementation): Best if your ECC processes are “broken” or highly customized. Start fresh by adopting “Clean Core” and standard best practices.

- Cost profile: Higher upfront consulting; lower long-term maintenance.

- Brownfield (system conversion): A technical “lift and shift.” Best if your current processes work well, you want to preserve historical data, and you’re under a tight timeline. It’s not ideal, but in certain situations, it’s the most feasible.

- Cost profile: Lower upfront; carries over technical debt.

- Bluefield/selective data transition: Carve out specific data or company codes.

- Cost profile: High complexity; requires specialized third-party tools (e.g., SNP or Natuvion).

4. Budgeting: Beyond the Software

A common mistake is budgeting only for licenses and the system integrator. Ensure your budget includes:

- Backfill costs: Budgeting for temporary staff to cover the “day jobs” of your SMEs while they work on the project.

- Data cleansing: SAP won’t fix your “bad data.” You may need a dedicated data project before the migration starts.

- Third-party integrations: Budget for updating tax engines (Vertex/Avalara), EDI, and WMS systems.

Phase 2: Implementation Planning and Resource Allocation

Timeline: 2–4 Months

Goal: Define the “Who” and “When.”

1. Assembling the Dream Team

You cannot rely solely on external consultants. Your internal team must include:

- Executive sponsor: A C-suite leader who can break ties when departments disagree on process changes.

- Process owners (SMEs): Your best people from finance, supply chain, and sales. If they aren’t “too busy” to be on the project, they probably aren’t the right people.

- Global process leads: Empowered individuals who can authorize moving from “custom” back to “SAP Standard.”

- Project Management Office (PMO): A PMO is a critical cross-functional team that can design and enforce a governance model and manage the execution of tasks, resources, deadlines, budgets, and change. An implementation is not just an IT project; it’s an integrated business transformation. A PMO can help remove blockers, secure approvals, and streamline global versus local decisions.

2. System Integrator Selection

Don’t just pick the lowest bidder. Evaluate partners based on:

- Conversion experience: Ask for references specifically for ECC to S/4 migrations, not just Greenfield builds.

- Accelerators: Do they have proprietary tools to automate custom code remediation or data transformation?

3. The ‘N+1’ Landscape Strategy

Planning your environments is a major cost and resource driver.

- Project landscape: You will need a sandbox, development, and QA environment for the S/4 project.

- Maintenance landscape: You still need to support your existing ECC system for 18 months.

- Strategy: Define how you will “double-maintain” (dual entry) transports between the old ECC world and the new S/4 project.

4. Data Purging and Archiving (The ‘Weight Loss’ Phase)

HANA is memory-intensive.

- Action: Implement an archiving strategy now. Identify “cold data” (7+ years old) that can be moved to a low-cost archive rather than the high-performance HANA database. This can reduce your infrastructure costs by 20–40%. It’s important to note that this action introduces its own level of cutover complexity.

5. Change Management Strategy

S/4HANA introduces the Fiori UI, which is a radical departure from the “Blue Screens” of ECC.

- Planning: Budget for a dedicated change management lead. This isn’t just training; it’s the strategy for how you will convince users that a new way of working is better, preventing shadow IT and resistance.

With the 2027 deadline fast approaching, your migration strategy should be a top priority. For expert planning, support, and implementation advisory, contact CrossCountry Consulting.

The 2026 Sage Intacct R1 release delivers high-impact enhancements designed to elevate automation and precision for finance departments. For administrators and power users leading digital initiatives, these updates streamline core operations, bolster internal controls, and significantly accelerate the month-end close.

Ready to maximize the value Sage Intacct can deliver to your business? View our demo of key updates:

Cash Management: Streamlined and Accurate

- Simplified check printing: Check printing is now easier to configure with a context-driven interface that eliminates unnecessary fields and streamlines setup for company address and logo. Key features include:

- Dynamic field display based on selections.

- Address fields only appear when selecting “Use a different address”.

- One-click logo uploads.

- Improved bank reconciliation with document numbers: A new Document Number field on Bank Interest and Charges now links fees with related transactions for better traceability. This improves bank reconciliation by matching payments and fees with shared identifiers, saving time, and improving audit trails.

- Unified transaction management: Imported bank transactions via Bank Transaction Assistant now flow directly to the Banking Cloud tab, consolidating all banking activity in one place and simplifying reconciliation workflows.

- Multi-entity bank register enhancements: Bank register report now auto-populates entity location filter within entities, saving time and reducing errors in multi-entity environments.

General Ledger: Advanced Reconciliation Capabilities

Organizations can now reconcile balance sheet accounts, tracking debit and credit activity systematically. High-value use cases include prepaid expenses, payroll clearing, accrued expenses, and fixed assets. The GL Account Reconciliations Activity report provides visibility into matched and unmatched transactions, improving accuracy and audit readiness.

Accounts Receivable: Better Customer Insights

Three new fields added to the customer record – health score, health status, and churn risk – allow teams to track customer account health. Use these insights for renewal risk identification, credit risk assessment, and prioritizing collections to improve revenue retention.

Additionally, new billing groups streamline recurring invoicing by allowing organizations to group customers with similar billing needs and automate invoice generation on a defined schedule. Teams can set start dates, limit occurrences, review invoices before posting, and monitor run results, including detailed errors. The feature supports non‑inventory items, requires future‑dated schedules, and includes new permissions for access control, reducing manual work while preserving flexibility.

Fixed Asset Management: Full Lifecycle Tracking

- Construction in Progress (CIP) support: CIP functionality tracks asset acquisition costs from initial spending through capitalization, streamlining visibility and transitions to active asset status.

- Asset cost adjustments: Teams can now adjust asset costs post-service using AP memos, addressing errors, capital improvements, or revaluations, with full transparency in the cost adjustments tab.

- Roll-forward reports: New roll-forward reports provide clear visibility into asset cost, depreciation, and net book value changes over periods, supporting GL to sub-ledger reconciliation.

- Flexible GL account assignment: Organizations can now assign the same GL account to multiple asset classifications, simplifying chart of accounts management.

End-to-end Sage Intacct value creation with an expert implementation and advisory partner

Simplify and transform financial management processes, automate key workflows for scale, and generate real-time enterprise insights for faster decision-making.

Tax Management: Simplified Reporting

- Enhanced VAT/GST display: Order entry and purchasing transactions now consolidate net amounts and tax totals into a single line for better clarity.

- Custom tax reports: Organizations can create tailored tax reports using configurable detail boxes and rules, streamlining compliance for jurisdictions with complex tax requirements.

Automation and Efficiency: Smarter Tools

- AI-powered import tools: Enhanced import capabilities include automated field mapping, data transformation, and preview functions, reducing manual data prep and improving accuracy.

- Predictive tax details: AP automation predicts tax details at the line level using historical trends, speeding up invoice processing and reducing errors.

- Secure email enhancements: A new allowed email addresses list strengthens security by ensuring outgoing emails originate from approved sources, reducing phishing risks.

- AP automation improvements: Improvements include auto-forwarding, broader file format support, and predictive text-based transaction creation, streamlining AP processes for high-volume operations.

- Bulk-update projects: Users can bulk‑update multiple projects at once, adjusting shared fields via a background job with email confirmation. Additionally, projects can link directly to CIP assets, automatically connecting transactions to streamline capitalization tracking and reduce reconciliation effort.

- Dynamic allocations: In the GL, a single allocation definition can now cover an entire account group and automatically include newly created accounts, minimizing maintenance for organizations managing large, multi‑entity expense structures.

Purchasing and AP: Advanced Tools

- Multi-currency close automation: Close automation is now supported for multi-base currency organizations, enabling faster, more reliable reconciliations globally.

- Line-level PO matching: Three-way matching now works at the line level for purchase orders, receivers, and invoices, improving accuracy and reducing manual intervention.

- Centralized AP advances: Multi-currency organizations can now manage AP advances at the top level, simplifying workflows and improving consistency.

- Recurring transaction notifications: Automatic email alerts notify teams of failed recurring transaction schedules, ensuring timely issue resolution.

Moving Forward

Sage Intacct R1 updates empower CFOs to optimize operations, improve controls, and gain strategic insights. Review the release notes and align features with your priorities in 2026 and beyond. CrossCountry Consulting’s Sage Intacct implementation experts can help you capitalize on the latest updates to maximize your investment. Contact us today to get started.

Private equity (PE) margin plans rarely fail because the math is wrong. They fail because the organization lacks a shared, operationally grounded view of how margin is created and destroyed – day to day, SKU by SKU, customer by customer.

As SKU economics become visible, leaders often realize that margin targets rely on price increases the market will not accept. In many situations, this leads the organization to debate assumptions rather than address root causes.

There is a practical way out: Make contribution margin the common economic language across finance, operations, and sales – then embed it into a contribution-driven KPI framework that refreshes at the pace of decisions.

The Trap: When the Model Is ‘Right’ but the Business Can’t Execute

Many manufacturing portfolio companies set margin targets at the top of the P&L (gross margin, EBITDA) ahead of SKU‑level cost and pricing visibility.

As soon as a reliable cost foundation is built – grounded in accurate bills of material, routings, labor standards, and overhead logic – the required price to hit the target can jump to levels customers simply won’t take. At that moment, the margin plan turns from a target into a source of internal friction.

This is the PE margin trap: Pricing is expected to close a gap that is largely driven by operational behavior and portfolio mix – not by commercial execution alone.

Why Pricing Gets Blamed

Pricing becomes the focal point because it appears to be the fastest lever. But when SKU‑level costing is transparent, pricing is effectively used to pass operational inefficiencies – overtime, low efficiency, scrap, and overhead – on to customers.

Sales teams can’t defend increases customers don’t value. Operations teams can’t change fundamentals overnight. Finance teams can justify the math, but the business still stalls.

The result is predictable: Leaders debate assumptions (OEE, labor rates, overhead burdens) instead of aligning on what must change and where it matters most.

Springing the Trap: Contribution Margin as an Operating Signal

The breakthrough is to treat contribution margin not as a finance output, but as an operating signal.

Contribution margin sits at the intersection of price, material, labor, and efficiency. It’s close enough to operations to be actionable and clean enough financially to guide decisions.

When contribution margin becomes the shared language, finance and operations stop debating who is “right” and start focusing on the few constraints and behaviors that actually move EBITDA and cash.

A Contribution-Driven KPI Framework (What It Is and What It Changes)

A contribution‑driven KPI framework makes clear how day‑to‑day operational decisions create or destroy economic value. Contribution margin reflects what remains after direct materials, direct labor, and variable manufacturing costs – showing how pricing, efficiency, and execution combine at the SKU and customer level.

Instead of optimizing activity metrics in isolation, teams use contribution margin to see where value is actually created: at constrained resources, within specific products, and across customers.

Optimally, the framework is delivered through near-real-time KPI dashboards (e.g., Power BI) that connect financial outcomes directly to operational drivers.

Characteristics of an effective framework:

- Clear, drillable views that flow from enterprise → plant → product family → SKU → customer.

- Explicit contribution margin components, showing how price, material cost, labor, and operational performance combine to drive contribution (in dollars and percent).

- A margin bridge that explains changes in contribution through price, volume, mix, and cost drivers.

- Operational KPIs translated into contribution‑based measures, so shop‑floor priorities align with economic impact rather than activity alone.

- Direct traceability to ERP and source‑system data, ensuring the insights are credible, explainable, and trusted.

Translating Plant KPIs Into Contribution-Lens KPIs

| KPI Area | Traditional KPI | Contribution-Lens KPI |

|---|---|---|

| Equipment | OEE% | Contribution per Machine Hour |

| Labor | Efficiency % / Utilization % | Contribution per Direct Labor Hour |

| Quality | Scrap % / FPY | Scrap Cost at Contribution |

| Throughput | Units per Hour | Contribution per Constrained Hour |

| Inventory | Turns / DIO | Cash Tied in Low-Contribution SKUs |

| Complexity | SKU Count | Contribution per SKU |

How the Framework ‘Springs the Trap’

Once contribution margin becomes visible and explainable, the margin plan becomes executable because leaders can sequence decisions instead of applying blunt force.

Here’s what a practical sequencing looks like:

- Short term: Protect contribution margin with targeted pricing actions and mix decisions where the economics are structurally strong.

- Medium term: Focus continuous improvement on the handful of drivers that destroy the most contribution at constrained resources (yield, labor, changeovers, downtime).

- Long term: Hardwire contribution margin insights into portfolio choices (rationalization, product innovation/PLM discipline, and capital allocation).

The Questions That Separate Aspiration From Execution

Instead of asking “Why can’t we hit the margin target?” leaders can ask questions that force clarity:

- Where is contribution margin being destroyed: price, material, labor, or overhead behavior?

- Which SKUs/customers consume constrained capacity but contribute the least value?

- Which operational improvements move the most contribution per constrained hour?

- What portion of the margin plan depends on improvements we have not yet made – and how will we measure progress weekly?

Strategic Value Creation From the Start

You don’t spring the private equity margin trap by pushing harder on price. You spring it by giving finance and operations a shared, contribution-margin view of reality – current enough to matter, clear enough to act on, and grounded enough to be trusted.

When contribution margin becomes the operating language, operational excellence stops being “efficiency theater” and becomes value creation.

CrossCountry Consulting helps sponsors and portfolio companies overcome the margin trap by restoring clear, actionable margin insight. Connecting SKU‑ and customer‑level economics to operational KPIs and working capital helps teams move from reactive financial analysis to proactive decisions that drive sustained improvements in margin and cash flow.

Contact CrossCountry Consulting to get started.

With audit season occupying so much time for financial reporting and audit teams, it’s easy to lose momentum after audits wrap up. But planning for a strategic, successful debrief is imperative. By making the most of this valuable opportunity, the post-audit debrief can be a productive, transformative exercise for the future, rather than just a review of past results.

Today’s Audit Progress Is Tomorrow’s Audit Efficiency

Even the most meticulous audits can benefit from a debrief. The best debriefs happen soon after the audit is completed, when pain points and ideas for future efficiencies are top of mind for everyone. Plus, a timely debrief allows financial reporting and audit teams to make investments over the traditionally slower summer months.

This time of reflection, ideally conducted between both internal management and your external audit team, allows you to identify areas for improvement and implement the types of technology and workflows needed to proactively avoid and address audit issues.

Using this time wisely can look differently for every organization. In addition to working through audit findings and implementing remediations, management teams should do the following:

- Gather feedback from all levels involved in the audit. Create an open and honest environment that allows everyone involved in the audit to provide their point of view. What worked? What didn’t? Take extensive notes and ask questions to understand the root cause of the issues. Analyze the volume, timing, duplication, and clarity of PBC requests. Streamlining requests and aligning them to the close calendar can significantly reduce audit fatigue and rework.

- Identify themes. Inefficiencies in an audit can typically be narrowed down to a few key themes. Are there communication issues that would benefit from a clearly defined schedule or standing status calls? Do certain processes or departments need dedicated attention?

- Develop an action plan. What are some of the top change priorities in the next several months? Who should own specific responsibilities and tasks moving forward? What are some benchmarks and milestones you’d like to achieve ahead of the next audit cycle? Make a plan with clear ownership, and then hold all parties accountable.

In our experience, here are three highly effective ways to capitalize on this phase of the audit journey:

1. Focus on Technology-Enabled Enhancements

As audit firms look to improve audit quality and efficiency amid rising regulatory scrutiny, there’s immense opportunity for management teams to proactively implement a modern data architecture to help achieve those very goals. While there’s obvious appetite for better use of technology in the audit process, it all starts with the quality of data. Adding more cloud-based systems or automation tools without addressing data concerns will add more IT bloat and potentially create more challenges.

To start, consider the source systems and flows of data. Tools like Snowflake can simplify data architectures and create a clean foundation for automating inefficient audit workflows and data compilation while maintaining traceability. Other platforms, like AuditBoard and Workiva, can help automate, visualize, and manage audit processes and enable decision-makers to surface risks before they reach the level of a deficiency.

Incorporate AI-Enabled Support

Many organizations are also now piloting GenAI and advanced analytics tools to accelerate audit readiness. These tools can help summarize supporting documentation, identify anomalies in large datasets, track PBC requests, and draft variance explanations.

During the debrief, teams should evaluate where AI reduced manual effort, where outputs required significant review, and what governance controls are needed (documentation standards, model validation, access controls) before expanding use in the next audit cycle.

By reducing reporting timelines now and going through several test runs of new technology-enabled reporting or audit workflows, the audit process at year-end can be less siloed, more flexible, and more enjoyable. Plus, the labor and time savings can help ease bandwidth and burnout concerns.

2. Implement a Control Rationalization Program

It’s often the case that, over time, auditors may recommend additional controls to be implemented. Sometimes, it’s healthy to step back and reassess the entire control environment to ensure the continual addition of controls isn’t causing more problems than it’s solving.

Control rationalization streamlines and validates controls to remove redundancies, overhead, and outdated frameworks. Building a rationalized control structure is a one-time investment that can save time in perpetuity for every future audit cycle – and the post-audit filing period is a prime opportunity to execute on this investment since tangible rewards will become evident in a matter of months and there’s more bandwidth to work on a project like this sooner versus later.

Rationalizing controls isn’t just a matter of adding or subtracting controls where necessary. It’s critical to deeply understand the process and risks of material misstatement, and then consider the types of controls necessary and how they can be organized more effectively and with less effort. For example, increasing your reliance on IT controls can reduce reliance on a number of manual controls; however, close attention must be paid to IT general controls.

Control rationalization will ultimately save labor and time in the long run but necessitates an investment today, along with proper implementation, training, and change management for maximum effect. Additionally, organizations should consider whether controls adequately address emerging risk areas such as cybersecurity, third-party/vendor oversight, and nonfinancial reporting processes (e.g., ESG metrics). These areas are increasingly reviewed by auditors and regulators and may require new or enhanced controls.

3. Conduct Interim Testing

In an audit, when you do the work matters. If aspirational audit projects from the summer are backlogged indefinitely, these tasks will only add to the mounting pile of work to complete during the end of the year. When optimizing the audit experience, the work should start months in advance of crunch time. While this may be standard for public companies with robust audit support, private companies may need to place added emphasis on a fast start, especially if this is their first time working this way.

Interim testing is a good practice for every firm to adopt. By evaluating and testing the company’s controls in advance, teams gain early insights into the effectiveness of the control environment.

This allows internal staff to potentially detect early control deficiencies and take corrective action before the actual audit. It also means, ideally, that auditors can spend less time doing detailed transaction testing at a later date, further reducing the risk of misstatements and improving the audit experience.

As David Moore, Co-Founder and CFO of MidCap Financial, noted in the video, it’s important to work with a strategic audit advisor on key projects to understand the latest thinking in the accounting industry, which can enhance audit process efficiency internally and when approaching external audit partners at a later date.

Interim testing requires both management and the audit team to plan in advance, which may include acceleration of certain processes and reallocating resources on both sides. Dedicated resources and accountability are key to making interim testing worthwhile – and additional external resources may be required to alleviate any internal workload concerns.

Leading organizations are also moving toward continuous control monitoring and rolling testing throughout the year rather than relying solely on traditional interim procedures. This approach distributes workload, reduces year-end pressure, and enables earlier identification of control gaps.

Maintaining Audit Agility

By making some of these enhancements in the coming months, it’s possible to execute every future audit more efficiently and with greater confidence in the outcome. Additionally, as evolving risks and regulations emerge, the tools and processes you put into place today should be adaptable.

When preparing action plans from the debrief, organizations should account for several shifts shaping audit readiness today:

- Expanded use of automation and AI in finance and audit workflows.

- Heightened focus on cybersecurity and data governance controls.

- Increased expectations around ESG and other nonfinancial reporting.

- Ongoing accounting and internal audit talent constraints.

- Hybrid and distributed work environments requiring stronger coordination.

Addressing these factors early can prevent recurring issues and position teams for a more efficient audit next year.

CrossCountry Consulting’s unique position as a technology-enabled audit advisor means our accounting advisory, risk advisory, and business transformation teams work cross-functionally to design, build, and deploy leading technologies that meet the objectives of auditors and management. Our audit specialists speak the language of auditors and take the burden off management teams by driving value at all points in the process before, during, or after an audit – wherever support is needed, we plug in.

To maximize your audit debrief period, contact CrossCountry Consulting.

Across finance organizations, automation and AI have shifted from experimental pilots to a strategic necessity. The leaders making real progress aren’t “doing AI” for its own sake – they’re building fluency, anchoring change in business goals, and starting with targeted, low‑risk processes that show results fast.

When leaders align the three pillars of people, process, and data with the appropriate governance, AI ROI can be visible in days or weeks, not years. To accelerate AI adoption and manage risks along the way, finance teams must evolve to be AI-fluent.

From Noise to Fluency

The most effective finance teams cut through AI hype by building organizational fluency first: a shared understanding of what automation is (and isn’t), how it will be used, and why it matters to the business right now. Fluency lowers resistance to change, encourages experimentation, and clarifies where automation can remove low‑value work so people can focus on higher‑value analysis and decisioning.

Fluency isn’t a one‑time training – it’s an ongoing practice. Leaders who communicate purpose early, invite feedback often, and celebrate quick wins create a durable change curve that outlasts any single tool or project.

Start Small, But Start Now

The best AI and automation programs begin with three to five low‑risk, high‑impact processes (for example, a repetitive reconciliation, a recurring reporting package, or a manual review task). Teams automate it, measure the outcome, and share the story internally to build momentum. This is CrossCountry’s Jumpstart AI methodology, and the approach compounds over time: each small win lowers the barrier for the next wave of improvements, which eventually lead to a larger finance transformation where clusters of agents can be created and deployed across common business processes. See it in action here: Jumpstart AI Adoption in Record-to-Report: A Practical Path for CFOs

In practice, this includes:

- Clear objectives and ROI analysis before technology selection.

- Process mapping to remove inefficiency prior to automation.

- Stakeholder alignment across finance, accounting, IT, and compliance teams.

- Phased rollouts with defined guardrails and KPIs.

What ‘Good’ Looks Like in 2026: People, Process, Data

- People: Upskill teams in analytics and AI literacy, and foster adaptability and critical thinking. Empower front‑line users to learn, test, and propose improvements. Recruit for curiosity and systems thinking as much as for tool‑specific experience.

- Process: Standardize and streamline before you automate. Design for controls, auditability, and compliance from day one. Treat AI projects with the same rigor as ERP or close‑accelerator implementations: objectives, owners, and measurable outcomes.

- Data: Treat the general ledger and subledgers as operational assets, not just reporting repositories. Push for transaction‑level granularity and consistent data models so AI can orchestrate workflows on the front end and surface insights on the back end. Invest in data governance and permissions from the start to reduce risk and speed audits.

Real‑World Momentum: Practical Use Cases

Leaders are already unlocking value by pairing targeted training with pragmatic pilots:

- Close and reconciliation automation: By connecting bank data and the GL, teams are achieving high match rates and substantially faster cycle times, and using AI to propose and refine rules. The human stays in control while throughput and consistency increase.

- Knowledge enablement behind the firewall: Organizations are consolidating SOPs and tribal knowledge into secure, searchable assistants that accelerate onboarding, reduce rework, and protect sensitive data.

- Natural‑language access to structured data: Instead of wrangling spreadsheets and dashboards, teams are asking direct questions of billing, customer care, and finance systems (“Who are our top 10 customers by December billings?”) and getting instant, governed answers.

The throughline: measurable efficiency gains without compromising control. When AI is positioned as an orchestrator – routing, proposing, and enforcing business rules – finance teams free capacity for analysis, business partnering, and scenario planning.

Explore strategic AI solutions that solve real-world problems

Align your AI strategy to business drivers, implement purpose-fit systems, and enable predictive analytics capabilities with the right governance, use cases, and technologies.

Managing Risk Without Slowing Down

Security and privacy concerns are valid and manageable. There are two complementary tracks:

- Enable safe experimentation: Provide enterprise‑licensed tools with clear data‑handling guidance (what’s in‑bounds vs. out‑of‑bounds), plus short “master class” sessions to help teams try, learn, and de‑risk.

- Productionize with governance: When pilots prove value, harden the solution: enforce role‑based access, integrate with source systems via supported connectors, and embed controls/monitoring in the workflow. The right vendor/partner should help make permissions and auditability first‑class citizens.

This balanced approach keeps velocity high while protecting sensitive information and preserving audit trails.

The Payoff: Better Decisions, Faster Scaling

With a clearer data foundation and AI‑assisted workflows, organizations can:

- Accelerate closes and audits with standardized, explainable outputs.

- Improve forecast quality by connecting operational drivers to accounting outcomes.

- Reinvest capacity from manual tasks into pricing, margin, and growth analyses.

- Scale efficiently without linear headcount increases while improving employee engagement by removing repetitive, low‑value work.

The Path Toward Org-Wide AI Fluency

Plan, pilot, and scale automation with confidence:

- Readiness and roadmap: Rapid assessments to prioritize use cases aligned to strategic goals, risk posture, and regulatory requirements.

- Process and control design: Standardize workflows and embed guardrails to ensure audit‑ready outcomes.

- Secure enablement: Stand up governed, behind‑the‑firewall AI capabilities and connect them to your finance tech stack.

- Change leadership: Build fluency with targeted training, communications, and a “start small, scale smart” playbook.

Bottom line: Automation is about progress, not perfection. Start with three to five processes, measure the impact, and build a culture that continuously looks for the next improvements. The organizations that cultivate fluency and align people, process, and data will lead the next wave of finance transformation.

To jumpstart your AI transformation journey, contact CrossCountry Consulting.

Defense programs in 2026 are advancing at unprecedented speed, and government officials continue to press contractors to increase production capacity and deliver more units faster. Networked satellites monitor assets in orbit. Autonomous systems and drones compress development timelines. Supply chains span advanced manufacturing, software, and hardware at scale.

In this environment, automation of back-office processes is no longer optional. As regulated technologies evolve, tolerance for supplier risk, manual controls, and fragmented data is eliminated.

Coupa’s FedRAMP-authorized spend management platform reduces risk by delivering a compliant, scalable way to onboard suppliers quickly, enforce three-way match consistently, and maintain regulatory controls without slowing the business. Manual, error-prone workflows are replaced with validated data, audit-ready records, and end-to-end automation from requisition through invoice, enabling companies to achieve compliance without sacrificing speed or agility.

Today’s Procure-to-Pay

CrossCountry Consulting combines deep experience implementing Coupa with hands-on knowledge of regulatory requirements for companies doing business with the government. Experience navigating FAR, CMMC, DFARS, purchasing system audits, and related requirements is applied during implementation to align procurement and finance operations with scalable, secure processes.

This platform-and-services combination is built for defense organizations that must scale procurement at mission speed while maintaining uncompromising compliance.

What defense leaders gain from modernizing Procure-to-Pay:

- Faster supplier onboarding without compliance tradeoffs.

- Standardized procurement across the business.

- Improved spend management with greater visibility into direct purchases across contracts and indirect spend, and the ability to track purchases by assigned categories.

- Improved cash flow with fewer invoice exceptions.

- Ability to maintain audit-ready documentation in a centralized, controlled repository.

- Better capacity utilization and working capital control from faster procurement and onboarding.

- A FedRAMP-ready foundation that scales with mission growth.

Explore expert Coupa solutions that solve real-world problems

Execute efficient Coupa deployments, enhance procurement and supply chain ROI, and minimize risk with Integration-as-a-Service offerings.

The Secret to Scaling Supply Chains: Automating the Mundane

Hypersonics and autonomous systems can seem easy with elite engineering talent. The ability to match parts to approved vendors, purchase orders, and invoices is where many programs slow down.

Defense innovation depends on controlling risk across suppliers, purchases, and payments. Back-office speed must match the pace of innovation, but speed without control introduces exposure.

Coupa’s FedRAMP-enabled platform allows companies doing business with the government to scale procurement and accounts payable without breaking controls. Integrations with PLM, CAD, MRP, and ERP systems ensure supply chain and manufacturing remain tightly governed while vendor onboarding and invoice matching move from manual to automated. Manual processes become systematic workflows with traceable audit trails, reduced rework, and faster cycle times. Compliance stops being a drag on execution and becomes part of how the mission is delivered.

The Real Bottleneck: Supplier Onboarding

Sometimes it seems easier to design an aircraft than to onboard a new supplier. This critical first step can involve numerous forms, approvals, and validations. Each day a supplier remains stuck in review, production slows, capacity utilization costs rise, and contracts face risk.

Coupa automates supplier onboarding through a single workflow driven by need, sourcing events, or integrated bills of materials. That workflow:

- Standardizes intake for banking, tax forms, and certifications.

- Automates approval routing to eliminate inbox bottlenecks.

- Ensures clear access controls for sensitive data.

- Creates a complete compliance record in one system on day one.

Coupa’s FedRAMP solution keeps data secure while accelerating onboarding timelines. Faster supplier activation directly supports mission execution.

Reducing Exposure by Eliminating Match Errors

Three-way match remains one of the strongest financial controls for companies doing business with the government. When purchase orders, receipts, and invoices align consistently, exceptions shrink, audits run smoother, and confidence in contract compliance increases.

Coupa’s automated FedRAMP solution applies built-in rules and logic that business users can maintain without IT involvement. Common exceptions are handled consistently and with accountability.

Coupa’s automated matching provides government contractors with:

- One version of the truth across purchasing, receiving, and invoicing.

- Fewer disputes and faster payment cycles.

- Reduced manual effort and rework.

- Reports and audit trails to ensure compliance at every step.

Small improvements within AP compound into real operational stability to ensure innovation isn’t slowed down by paper pushing.

Fast-Tracking Procure-to-Pay in Government Contracting: Case Study

CrossCountry’s implementation model, developed from more than 900 Coupa projects, is designed to help clients move quickly while navigating complex compliance requirements.

One of our high-tech defense clients helps companies analyze and act on complex data in high-stakes situations, but internally, they struggled with slow supplier onboarding, frequent AP errors, and compliance challenges. By implementing Coupa’s FedRAMP-authorized platform, the company:

- Cut supplier onboarding time.

- Reduced AP cycle times and disputes.

- Achieved centralized, audit-ready compliance records.

Finance teams shifted focus from paperwork to mission priorities, helping the organization innovate and grow.

Why FedRAMP Matters for Scale

With increased emphasis on cybersecurity compliance, government contractors can’t compromise on security. With FedRAMP authorization, Coupa provides a cloud platform designed for regulated environments and capable of handling covered defense information.

From Day 1, Coupa brings the level of control expected in regulated environments.

- FedRAMP-authorized cloud infrastructure.

- Security roles aligned to data sensitivity and access eligibility.

- A single, auditable record across procurement operations.

For organizations operating at extreme speed, retrofitting security can stall growth. With Coupa, security is foundational rather than reactive.

Getting the Implementation Right

Government contractors operate under different constraints. Governance is rigorous. Risks must be addressed early.

CrossCountry Consulting focuses on the practical details that make automation work in regulated environments, including:

- Matching alignment between Coupa and ERP.

- Clear definition and distinction of direct and indirect purchasing workflows.

- Restricted material rules embedded in process stages.

- Supplier compliance integrated at onboarding.

- Structured change management, RAID discipline, and decision ownership.

What Fast-Growing Contractors Gain

When procurement is automated with the right structure, growth accelerates.

- Suppliers onboard in days, not weeks.

- Audit readiness becomes continuous.

- Working capital improves through faster invoice processing.

- Teams focus on mission priorities instead of administrative work.

The organizations defining the future of defense aren’t waiting for supply chain friction to slow them down. They’re modernizing now, not after they stall.

Coupa provides the platform built for mission speed. CrossCountry Consulting ensures it’s designed to thrive in the realities of government contracting. Contact CrossCountry Consulting today for a Coupa readiness assessment.

The software/system development lifecycle (SDLC) has taken on even greater significance in recent years due to the proliferation of digital tools used in virtually every facet of modern work. Today, finance, accounting, risk, operations, HR, IT, and customer-facing functions, for example, are powered by an ecosystem of cloud-based platforms, automated technologies, and digital assistants.

As a result, system development projects have evolved from isolated IT initiatives into business-critical, compliance-sensitive efforts that impact every corner of the organization. With AI and digital transformation investments accelerating, the stakes for getting system implementations right have never been higher. However, roughly 70% of large-scale transformations fail to achieve their intended outcomes.

The Internal Audit Opportunity

Increasing regulatory demands, especially around SOX compliance, mean that failures can have material impacts on financial reporting and reputation. At the same time, the pace of innovation driven by AI, automation, and new development methodologies creates both opportunity and risk.

Internal audit teams are uniquely positioned to help organizations navigate this complexity. By moving from a traditional, post-mortem assurance role to a proactive, strategic partnership, internal audit can embed risk management and controls throughout the SDLC. To drive better outcomes, reduce surprises, increase business alignment, and provide transparency for senior leadership, internal audit has a critical role to play.

The New SDLC Reality: Rapid Change and Increasing Complexity

Adding value to the SDLC requires a forward-looking approach that anticipates complexity and addresses risk across these essential areas:

- Dynamic tools and technology: Organizations are navigating an expanding ecosystem of technology and tools to support every phase of digital transformation and SDLC initiatives. This environment increases the need for a strong data foundation, centralization, and reporting to deliver meaningful analytics, KPIs, and metrics to key stakeholders.

- AI and automation: Teams are expected to deliver more with less and faster. Automation and AI can accelerate innovation, but they also introduce new risks if control design isn’t keeping pace. To capture value safely, organizations need a clear AI strategy that embeds governance, control design, and ethical considerations into every stage of development.

- Tailored methodologies: The starting point should never be yesterday’s waterfall, agile, or DevOps playbook. It should be a deliberate decision informed by governance, risk, and value realization. By treating methodology as a strategic choice rather than a default, companies can ensure that technology investments drive transformation outcomes, not just project completion.

- Third-party risk: Whether you’re leveraging external tools to build or implement purchased software, third-party risk often goes under the radar during project execution. Organizations must move beyond ad-hoc vendor checks and embed third-party risk considerations into an integrated risk management framework. This means assessing vendor security, compliance, and operational resilience alongside internal controls, ensuring that external dependencies don’t compromise project outcomes.

Effective assurance requires aligning technology strategy to business activities within the organization. Controls should be designed and tested to fit the real-world process, not just the theoretical model.

‘Shift Left’: The Case for Early and Continuous Internal Audit Engagement

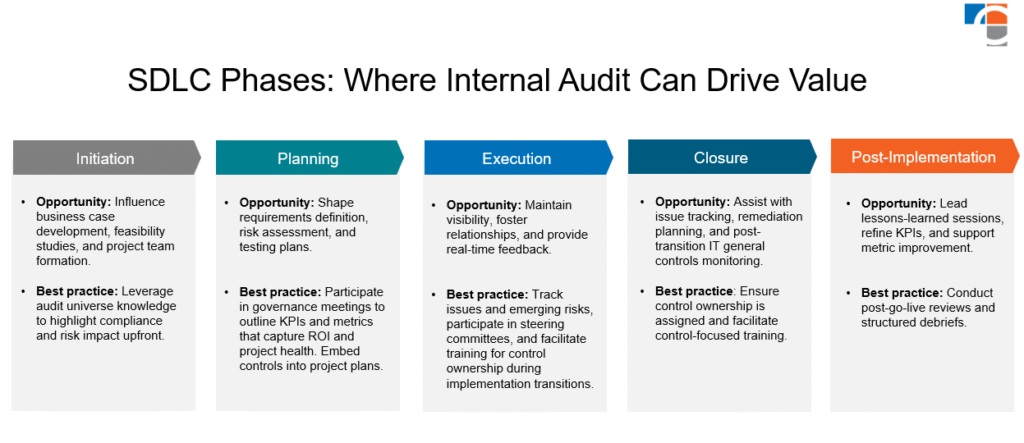

The earlier internal audit is involved in the SDLC, the greater the impact. Waiting until implementation means missed opportunities to influence design, governance, and risk mitigation. Internal audit’s value is maximized when it “shifts left,” engaging early and often and becoming a trusted strategic partner to management and the executing teams in risk identification and control implementation. Visualized below are some of the key opportunities and best practices for internal auditors to make a demonstrable impact during each phase of the SDLC:

Elevate the Impact of Your Internal Audit Function

Internal audit’s expanded role in the SDLC is a strategic advantage. By engaging early, embedding controls, and partnering with stakeholders, internal audit can drive project success, strengthen compliance, and deliver measurable business value.

Ready to shift left? Connect with CrossCountry Consulting to learn how your internal audit function can become a true partner in system development.

The Coupa R44 release brings a mix of platform-wide enhancements, procurement efficiencies, and critical security updates that every administrator and power user needs to know. Want to explore all things R44 in more detail? Watch our recent webinar.

And for more information on some of the key changes in R44, CrossCountry Consulting’s Coupa implementation and transformation experts have distilled several to focus on:

Key Dates and Release Waves

Coupa has structured the R44 rollout across three specific waves for production environments.

Production Release Schedule:

- Wave 1: January 16, 2026

- Wave 2: January 23, 2026

- Wave 3: February 6, 2026

Understanding this schedule is vital for ensuring your team has adequate time to test new features in sandboxes before they hit live environments. For enterprise clients with Premier support, Wave Zero (December 8, 2025) offers an early preview in test environments. This “early access” group helps vet features before broader release. For most organizations, however, we recommend targeting Wave 1 for test environments and Wave 3 for production. This strategy provides the longest runway to validate workflows and troubleshoot any potential issues before they impact daily operations.

Maintenance and Daily Updates

Beyond the major release waves, Coupa is more aggressively including features in its maintenance updates. These updates, occurring every two weeks after a major release, often include smaller but impactful features. Additionally, daily updates provide regular bug fixes.

To stay on top of these frequent changes, ensure your user record has the Upgrade Administrator role assigned. This role guarantees you receive direct notifications from the environment regarding when these specific updates will land, complete with links to detailed release notes.

GPG File Transfer Encryption Cipher Deprecation

Security remains a top priority in R44. A critical update in this release involves the deprecation of older, less secure encryption ciphers for GPG file transfers. Starting with the January 2026 release, Coupa will exclusively support AES256 or stronger ciphers.

Why this matters: This change specifically impacts file-based integrations. If your organization relies on older encryption methods for exchanging files with Coupa, those integrations may fail if not updated. Note that this generally does not affect corporate card integrations (like Visa or Mastercard), as those providers typically already adhere to higher security standards. However, for other custom file-based integrations, it’s imperative to verify your encryption settings now to avoid service disruptions.

Explore expert Coupa solutions that solve real-world problems

Execute efficient Coupa deployments, enhance procurement and supply chain ROI, and minimize risk with Integration-as-a-Service offerings.

Multi-Factor Authentication Support

As part of Coupa’s rollout of the Coupa Identity Provider, R44 introduces support for Multi-Factor Authentication (MFA) for users logging in via username and password (Non SSO/SAML login).

While this rollout is managed and currently limited to a small number of customers, it signals a broader shift toward tighter security protocols. Once enabled, users accessing the platform directly will be required to enroll in MFA using applications like Google Authenticator or Microsoft Authenticator. This is distinct from the step-up authentication used for high-risk actions (like changing payment details) and focuses specifically on the initial login process.

Procurement and CSP Enhancements

R44 isn’t just about backend maintenance. It also delivers tangible improvements for procurement teams and suppliers.

Workbench Tasks

New tasks in the Unified Workbench bring visibility to issues that previously required digging into specific tables. You can now resolve Purchase Order transmission failures (both email and cXML) and cXML ASN errors directly from the Workbench. This centralization streamlines troubleshooting and ensures critical documents don’t get stuck in limbo.

AI Suggestions for Requisitions

Building on R43, R44 enhances the “Pending Buyer Action” stage. When enabled, AI can suggest missing field values, such as commodity or contract, based on historical data. This allows buyers to apply updates individually or in bulk, significantly speeding up the requisition approval process without consuming AI credits.

Supplier Portal Controls

For suppliers, R44 introduces tighter controls within the Coupa Supplier Portal (CSP). New permissions allow supplier admins to restrict who can manage payment methods. Additionally, the “Remit-To Address” has been removed as a standalone payment method option during onboarding, forcing a cleaner data structure under Legal Entities. This change reduces confusion and prevents the creation of duplicate or erroneous remit-to records.

Stay Informed

With the pace of updates increasing, proactive management is key.

- Check your wave: If you’re unsure which wave your production environment is assigned to, open a ticket with Coupa support.

- Review integrations: Audit your file-based integrations for compliance with the new encryption standards.

- Enable key features: Many enhancements, such as the Workbench tasks and AI suggestions, are “opt-in” and require configuration in the Company Information setup.

A proactive approach today will prevent disruptions and unlock the full potential of the new release. For hands-on Coupa expertise and maximum value from R44, contact CrossCountry Consulting.

ESG’s New Reality

ESG reporting has shifted from voluntary, narrative-driven disclosures to regulated, data-focused disclosures. New rules, like California’s SB 253 and the EU’s CSRD, along with increased stakeholder scrutiny, now require sustainability information to be complete, consistent, and reliable.

Limited assurance is evolving to the baseline standard for sustainability-related data, providing users with greater confidence in the reported data. This trend is particularly evident in climate-related disclosures. California’s SB 253 mandates large companies to report greenhouse gas emissions (Scopes 1, 2, and 3), with assurance requirements phased in over time, as summarized below.

| GHG Emissions Scope | Reporting Deadline | Assurance Requirement |

|---|---|---|

| Scope 1 (direct) | 20261,2 | – Limited assurance expected by 20273 – Reasonable assurance expected by 2030 |

| Scope 2 (indirect from purchased energy) | 20261,2 | – Limited assurance expected by 20273 – Reasonable assurance expected by 2030 |

| Scope 3 (indirect upstream and downstream across the supply chain) | 2027 | – Without assurance in 2027 – Limited assurance by 2027 |

1As of 2025, and following stakeholder feedback, CARB is proposing a first-year-only reporting deadline of August 10, 2026.

2CARB clarified that entities with fiscal year-ends between January 1, 2026, and February 1, 2026, will report on data from the fiscal year ending in 2026, while entities with fiscal year-ends between February 2, 2026, and December 31, 2026, will report on data from the fiscal year ending in 2025.

3CARB has clarified that it will exercise enforcement discretion for first-year reporting in 2026, meaning companies may submit Scope 1 and Scope 2 emissions data based on the information they already had or were collecting when the enforcement notice was issued, even if that data has not undergone limited assurance.

What Does Limited Assurance Actually Mean?

Limited assurance is a moderate level of confidence provided by an independent assurer over the sustainability-reported data and quality of reporting. In practice, this means the assurer performs targeted procedures such as analytical reviews, interviews, and selective testing to determine whether anything suggests the information is materially misstated.

Unlike reasonable assurance (think: full financial audit), the work is narrower in scope but still requires transparent, well-defined processes. However, “limited” does not mean “light.” Assurance providers still expect structured processes, defensible methodologies, clear ownership, and effective governance, along with clearly documented assumptions, consistent calculation methods, and evidence that management can confidently substantiate how each metric was developed and whether the resulting metrics are reasonable. Although controls are generally not tested during limited assurance, a strong control environment plays a critical role in supporting the completeness and accuracy auditors look for in the reported information.

Essential Steps for Assurance Readiness

With a practical, step-by-step approach, organizations can strengthen assurance readiness. The steps below define a clear path to limited assurance preparation:

1. Clarify Scope and Ownership

Clear roles and scope help prevent reporting errors and increase auditor confidence in ESG oversight.

- Identify which ESG disclosures fall under limited assurance (e.g., GHG emissions, workforce metrics, value-chain data).

- Clearly define boundaries to avoid gaps or ambiguity in what must be reported.

- Assign ownership across sustainability, finance, risk, internal audit, IT, and operations to ensure accountability and active governance.

2. Assess Current Maturity

Early discussions with SMEs and auditors help identify high-risk areas and remediation priorities before formal assurance begins.

- Review current data collection processes for completeness, consistency, and auditability.

- Evaluate existing documentation, calculation methods, assumptions, and controls to understand your true readiness level.

Explore expert ESG Reporting solutions that solve real-world problems

Integrate sustainability reporting best practices and build an ESG framework that meets current and emerging regulatory requirements.

3. Strengthen Governance and Controls

Effective governance frameworks allow ESG information to withstand independent scrutiny.

- Establish formal ESG policies, procedures, process documentation, and oversight mechanisms that mirror the rigor of financial reporting.

- Align ESG controls with SOX-like principles like segregation of duties, documented review and approval processes, evidence retention, and escalation protocols to ensure consistency and reliability.

4. Test, Refine, Prepare

Early testing reduces surprises during the formal assurance engagement and accelerates readiness.

- Conduct mock or dry-run assurance reviews to identify weaknesses early.

- Use findings to develop targeted remediation plans, refine data, enhance documentation, strengthen methodologies, and improve audit trails before auditors arrive.

These four steps establish the foundation for credible, repeatable ESG reporting under assurance. While limited assurance may be the starting point, the disciplines required to achieve it set organizations up for longer-term regulatory resilience, and as ESG reporting matures, limited assurance will eventually evolve into reasonable assurance. By approaching assurance readiness as a journey rather than a one-off exercise, organizations can reduce audit friction, build stakeholder confidence, and position themselves for the increasing scrutiny that lies ahead.

Accelerate Readiness Today

Translating assurance requirements into operational reality is where many organizations encounter complexity. ESG data cuts across functions, systems, and geographies, often without the benefit of mature controls or standardized processes.

CrossCountry Consulting is uniquely positioned to guide organizations through the complexities of ESG assurance readiness. Our team delivers:

- Deep expertise in sustainability, financial reporting, and risk advisory.

- Tailored solutions that meet both regulatory requirements and strategic objectives.

- Targeted training for management and internal teams, fostering ESG awareness and embedding compliance into daily operations.

- Technology enablement for data management and evidence trails, helping automate and streamline ESG processes.

To accelerate your ESG assurance readiness with the partnership of a strategic ally, connect with CrossCountry Consulting.

Sage Intacct is designed to evolve alongside your business. With quarterly product releases and continuous innovation, organizations that actively manage and optimize their Sage Intacct environment consistently realize greater efficiency, stronger reporting, and a higher return on investment.

Yet many organizations still approach Sage Intacct reactively – adopting new features sporadically and relying on legacy configurations that no longer reflect how the business operates. Ensure your Sage Intacct ERP scales with your organization with these best practices:

1. Establish a Quarterly Sage Intacct Release Management Process

Sage delivers new functionality every quarter across financial management, reporting, automation, and integrations. Without a structured review process, valuable enhancements often go unused.

Best practice: Implement a formal quarterly release review that includes:

- Reviewing Sage Intacct release notes relevant to your modules.

- Evaluating new features against current pain points.

- Identifying process, reporting, or automation opportunities.

- Assigning clear ownership for adoption and change management.

Organizations with a defined release management process are better positioned to reduce manual work, avoid unnecessary customizations, and stay aligned with Sage’s product roadmap.

End-to-end Sage Intacct value creation with an expert implementation and advisory partner

Simplify and transform financial management processes, automate key workflows for scale, and generate real-time enterprise insights for faster decision-making.