Regional banking institutions evaluating new ERP or EPM systems often focus on improving how transactions are captured, closed, and consolidated within the Record-to-Report process. When the emphasis centers on general ledger design and system implementation, reporting strategy is frequently addressed too late in the process.

Yet the largest consumers of financial information are rarely considered early in technology design and implementation. Reporting strategies must support regulatory reporting across agencies such as the FDIC, Federal Reserve, and SEC, while also enabling internal management reporting across financial performance and operational activity. When implementations focus primarily on ledger design and transaction processing, the needs of these reporting stakeholders are often addressed too late.

This raises an important question: how should financial institutions design reporting architecture that meets the needs of all stakeholders from the beginning, rather than retrofitting solutions after an implementation is already underway?

The answer is to anchor system design in reporting requirements from the start. Instead of treating reporting as a downstream output of the general ledger or EPM platform, institutions must first define the reports they need to produce—from regulatory filings to board materials and profitability analyses—and then design the supporting data architecture accordingly. While formats may differ, all reporting should be drawn from consistent, multi-dimensional, and governed source data. Without that foundation, even the most advanced platforms simply accelerate existing fragmentation rather than resolve it.

Neglecting Reporting During Implementation

Across institutions, as much as 75% of resource time is spent gathering, reconciling, and validating data rather than analyzing it. Instead of enabling insight and automation, finance teams devote significant effort to manual processes across fragmented data sources simply to produce required reporting.

This misallocation of effort begins with a single misstep: treating reporting as an afterthought. When reporting requirements are not defined upfront, “shadow reporting” is developed to fill the gap. Regulatory, management, and statutory outputs evolve along separate paths, creating data silos without a single version of the truth producing unreliable data and increasing operational reporting risk.

Reversing this pattern requires more than incremental fixes. It requires designing reporting architecture deliberately, with clear multi-dimensional structure, governed data foundations, and defined methodologies from the outset. Only then can institutions redirect effort away from reconciliation and toward insight.

Crafting a Holistic Reporting Strategy

Institutions must also support multiple categories of reporting, including regulatory reporting (SEC, FINRA, FDIC/Federal Reserve), management reporting (business reviews, board reporting, ALCO), and other internal reporting across accounting, tax, credit risk, and operations. While these reports serve different audiences, they are largely derived from the same underlying data at varying levels of granularity.

The starting point for these institutions is to catalog the full inventory of required reporting and define the data outputs necessary to support each use case, with a clear focus on delivering value to the end user. Once defined, the reporting strategy becomes a north star, guiding the evolution of reporting capabilities as well as supporting data and technology infrastructure. When aligned properly, this foundation enables institutions to meet all reporting needs from a single version of the truth, driving consistency, efficiency, and more meaningful insight.

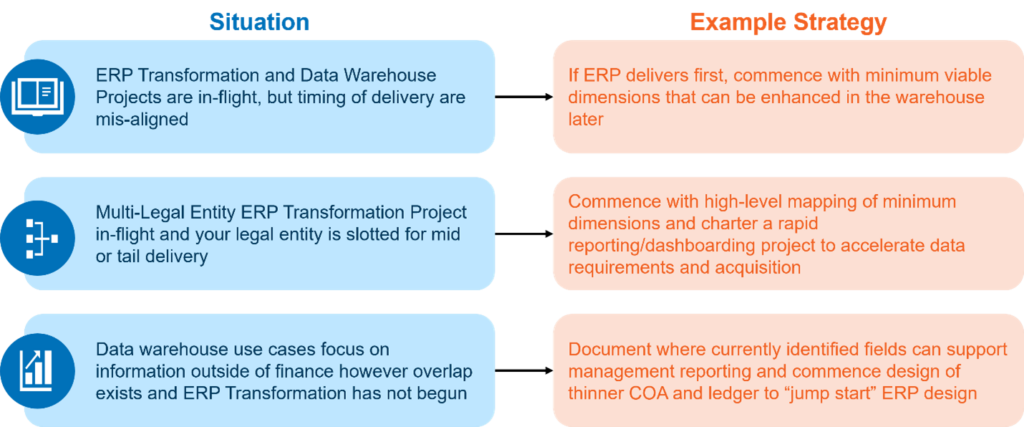

When planning a reporting strategy, it is important to consider the different timing scenarios that may arise. An example of common situations and related strategies include:

It’s not uncommon for institutions to define target and interim states to deliver value on an incremental and manageable basis. Typical timelines range from 3-24 months, delivering notable functionality on a quarterly/semi-annual basis.

Single Version of The Truth

Achieving a single version of the truth begins with rethinking the data foundation. While the general ledger is essential for financial reporting, it is inherently too summarized to support deeper strategic insight.

The path forward is to establish an instrument-level foundation that captures transaction detail at its natural level of granularity, including loans, deposits, securities, and other financial products. From there, dimensions must be harmonized across the enterprise so that regulatory and management reporting draw from the same governed data source.

When reporting frameworks originate from a common foundation, reconciliation becomes embedded in the architecture rather than dependent on manual effort. The result is a reporting environment that supports statutory requirements while remaining flexible enough to generate meaningful business insight.

Optimizing Reporting for Strategic Insights

Once the data foundation is in place, the focus shifts from assembling numbers to generating insight. For regional banks and diversified financial institutions, this means moving beyond static P&L statements toward multi-dimensional reporting.

The most meaningful insights emerge when performance can be evaluated across consistent enterprise dimensions. At a minimum, institutions should be able to analyze activity by Customer or Client, Product, Account, Organization, at the Instrument level, and at intersections across enterprise dimensions. By examining these dimensions, leaders not only gain insight into the numbers themselves but also uncover the reasons behind their changes and identify where genuine value is generated.

Achieving this requires more than layering attributes onto the general ledger. Each dimension must be defined, governed, and structured hierarchically so that activity rolls consistently from instrument to product, product to line of business, and into enterprise reporting without manual reclassification. When that structure is in place, finance, risk, treasury, and regulatory reporting can view the same activity through different lenses.

That is what transforms reporting from a compliance obligation into strategic analytics that drive business objectives.

The Reporting Landscape

Financial institutions operate in one of the most complex reporting environments of any industry. Regulatory filings, statutory financials, and internal management reporting each impose distinct structural requirements and levels of granularity, and none map cleanly across reports or to the general ledger. Regulatory reports such as the Federal Reserve Y-9C or FDIC Call Report require highly specific classifications and cross-report integrity, while management reporting demands flexible views across clients, products, segments, and business lines.

These requirements rarely align naturally with the structure of the general ledger chart of accounts. Without intentional design, institutions typically resort to developing parallel reporting processes for regulatory, statutory, and management outputs, increasing reconciliation effort and operational risk.

The objective of a modern reporting architecture is not to eliminate multi-dimensional reporting differences, but to anchor them to a common data foundation. When reporting frameworks draw from the same governed source of instrument-level data, institutions can satisfy multiple reporting obligations while preserving transparency, consistency, and reconciliation across report outputs. The same loan can satisfy a Call Report schedule, an FRB submission, or an SEC maturity bucket disclosure simply by applying the right attribution logic — no separate pipelines required.

This foundation becomes especially important when management reporting evolves beyond financial statements into profitability and performance analytics.

The Role of Management Accounting Methodologies

With a consistent reporting architecture in place, institutions can move beyond producing numbers to understanding performance. This is where management accounting methodologies become critical.

Multi-dimensional profitability and planning are only as credible as the methodologies that support them. When poorly designed or inconsistently applied, business lines lose confidence in the numbers, and management reporting stops driving decisions. Four areas consistently distinguish institutions that generate meaningful insight from those that do not.

Funds Transfer Pricing (FTP)

Without a disciplined FTP framework, business lines appear more or less profitable than they actually are. FTP transfers interest rate and liquidity risk to a central function where it can be properly managed, leaving business lines with a stable, comparable margin that reflects true commercial performance.

Expense and Cost Allocation

When costs are not allocated to the deal or instrument level, product profitability becomes guesswork and accountability breaks down. A well-designed allocation model assigns costs based on actual consumption and rolls them into meaningful product and business-line views. Whether an institution allocates fully or excludes corporate overhead matters less than making that decision deliberately and applying it consistently.

Revenue Sharing and Allocation

In relationship-driven institutions, deals frequently involve multiple teams. When attribution rules are not defined upfront, disputes inevitably follow. Upfront sharing, ongoing splits, and double-counting each create different behavioral incentives and reporting outcomes. Establishing clear governance around revenue attribution is therefore as much a cultural decision as a technical one.

Capital Allocation

Business lines that do not bear the cost of capital have little incentive to use it efficiently. Allocating regulatory capital to products and lines of business, and measuring returns against that cost, allows institutions to evaluate performance in terms of shareholder value rather than revenue alone. As with other management accounting methodologies, capital allocation must balance analytical precision with decision-making value and long-term maintainability; excessive granularity can add complexity without improving insight.

Governance and Transparency

The fastest way to undermine any of the accounting methodologies is opacity. When business lines cannot explain how allocations are calculated, they quickly stop trusting the results. Tying charges to understandable activity drivers—accounts serviced, transactions processed—transforms allocation from a political debate into a practical tool for running the business.

Technology-Enabled Reporting Done Right

The journey to optimized reporting and analytics is not simply a technology upgrade. By building reporting frameworks rooted in instrument-level data, governed multi-dimensional structures, and disciplined management accounting methodologies, regional banking institutions transform how the finance function operates and delivers value to the organization.

Teams that once spent as much as 75% of their time gathering and reconciling data can redirect that effort toward generating insight and informing decisions. For institutions seeking to scale, this shift represents a meaningful and sustainable competitive advantage.

The institutions that define their reporting and analytics strategy at the beginning of a transformation position themselves to extract far greater value from ERP and EPM investments. CrossCountry Consulting helps financial institutions develop these strategies to deliver scalable insight, stronger governance, and long-term business value.