With the environmental, social, and governance (ESG) investment market expected to reach $50 trillion by 2025 – up from $35 trillion in 2020 – ESG investing and ESG strategy have become mainstream.

And it’s not just profitability and access to capital that are driving organizations to invest in ESG funds and initiatives – though these factors are indeed key. Consumers and employees are primary motivating factors as well.

As internal and external forces demand greater ESG transparency from corporations, regulatory bodies like the SEC are enhancing disclosure requirements for public companies.

ESG frameworks are taking shape, including governance structures. Three potential governance models that will help companies shape their ESG initiatives are:

- Meet: Doing the bare minimum to satisfy regulatory requirements.

- Exceed: Adhering to baseline regulatory requirements + plotting out a medium-term vision of where the organization plans to be.

- Lead: Weaving sustainability into all future strategic goals of the organization in addition to complying with regulations.

Choose Your Own ESG Destiny: Meet, Exceed, or Lead Governance Frameworks

A governance model can chart an organization’s current and future approach to enhancing ESG performance, managing ESG risk, and communicating ESG goals in a cohesive, mission-driven way.

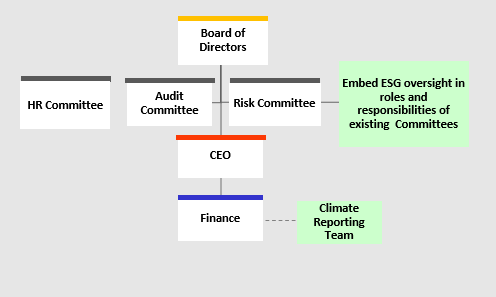

Meet

The Meet model draws on a firm’s existing leaders and committees instead of new cohorts specially dedicated to ESG. This first governance framework is a viable model for companies that are confident in their committees’ existing ESG expertise.

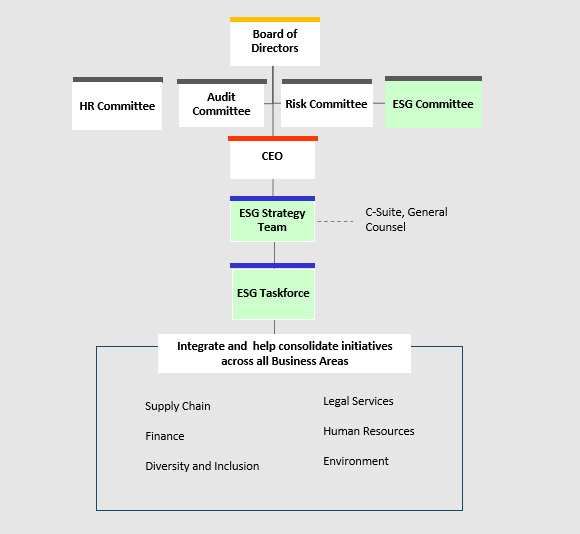

Exceed

The Exceed model goes a step further by establishing a board committee specific to ESG as well as a dedicated ESG strategy team supported by an ESG task force. It is leadership’s responsibility to integrate ESG across their respective business units.

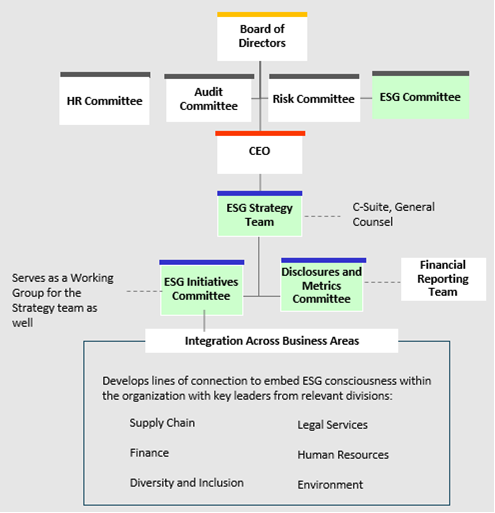

Lead

The Lead model further delegates ESG responsibilities by establishing subcommittees with a defined focus on two key ESG components: initiatives and metrics. The Lead model distinguishes itself by asking leaders across business areas to take an active role in ESG strategy conversations.

Consider ESG Questions and Resources

There isn’t a one-size-fits-all approach to designing an ESG governance framework, but commonalities certainly exist among the myriad challenges companies face.

Questions

For example, prevalent questions when embarking on an ESG governance journey include:

- Who should lead the effort?

- Can an existing board or committee oversee the effort?

- Do we need a Sustainability Officer?

- Which stakeholders should have a seat at the ESG governance table?

- Should a task force be created?

- Should the take force report to the CEO, CFO, or someone else?

- Is an incentive structure needed?

Resources

To be an industry leader in ESG requires capital investments and total alignment throughout all levels of the organization. Not all firms are prepared for this kind of commitment. Hence many companies will settle for the bare minimum in the interim while waiting to see how their industry (and the SEC regulatory requirements) evolves.

When examining potential ESG resources, the below factors come into play:

- Stakeholder priorities: Consider top priorities of an organization’s key stakeholders. This will drive the support to execute.

- Regulatory timeline: Larger public companies are expected to comply by the 2023 fiscal year, while smaller public companies and private companies will have a slightly longer road to ensure compliance.

- Existing board structure, board committees, and skill sets: Evaluate the current board structure and skill set of its members to find the right place for ESG oversight.

- Current reporting lines in an organization: Evaluate if you can leverage any of the existing reporting lines, especially bottom to top.

- Current sustainability activities: Assess and consolidate sustainability activities already underway.

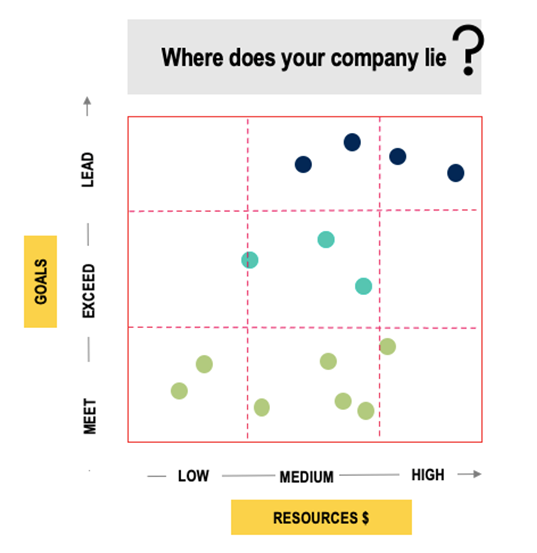

In the below matrix, the loftier the ESG goal, the more intensive the resource required. Firms must be realistic in what they’re capable of allocating to ESG when setting goals that staff, investors, and customers can believe in – and that regulators can verify.

Are Organizations Ready for Heightened ESG Scrutiny?

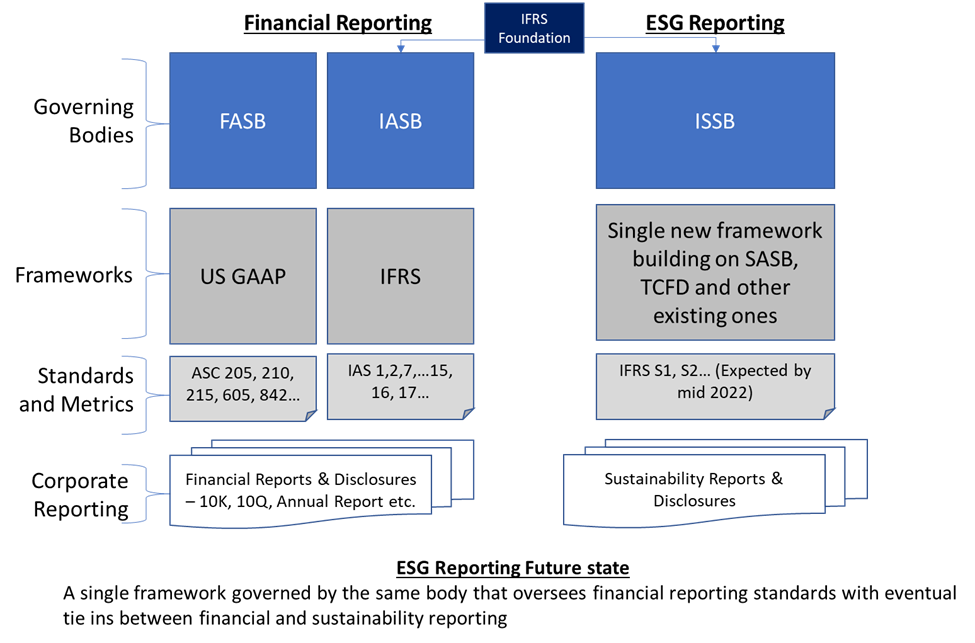

ESG reporting standards are beginning to mirror financial reporting standards in methodology and governance, as evidenced by the formation of the Sustainability Accounting Standards Board (SASB) and the International Sustainability Standards Board (ISSB). Organizations with proactive, successful financial reporting frameworks thus have an advantage when applying these practices to the world of ESG reporting.

Not every firm has this foundational base of talent, knowledge, diligence, and corporate governance, however. Enhanced ESG disclosure will likely prove to be a substantial ongoing challenge.

Additionally, a recent proposal from the SEC suggests it intends to require climate-related disclosures from registered companies in the not-so-distant future. The regulatory agency estimates it will cost large organizations about $644,000 annually to comply with the requirement. While regulators’ cost predictions tend to underestimate the spend required to implement new rules, the SEC does expect ongoing yearly compliance costs to drop to $530,000.

Of course, these requirements pertain to public companies in the near term. Compliance and governance frameworks will be relevant to private firms as well, as SEC rules evolve over time.

Constructing a framework to ingest, analyze, verify, and report key ESG metrics is step one to getting ahead of the compliance curve. Firms capable of compiling ESG data may still find it difficult to produce an annual report, map ESG goals to specific ESG criteria, or truly drive investor, customer, and employee confidence. Clearly, much work lies ahead.

For expert support in designing and executing an ESG governance framework, contact CrossCountry Consulting.